Wrongful Foreclosure Module 5

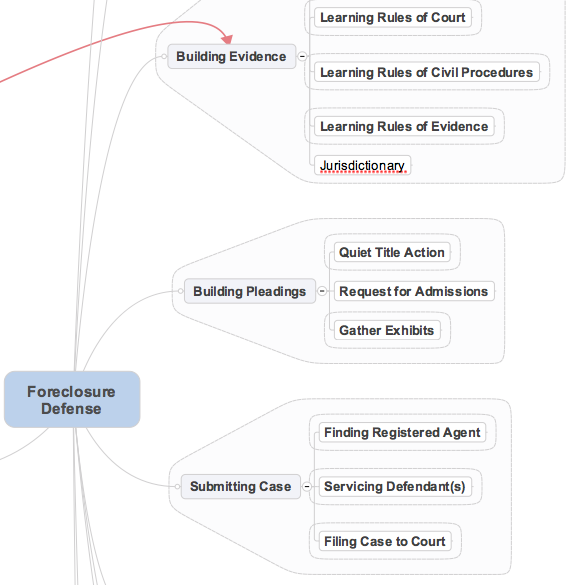

Building Your Case

In the last module, we talked about how you gathered evidence in support of your case. It was pretty heavy lifting but I hope you fully understand what we are trying to do.

In this module, we will be building your case.

Here are a couple of important documents for you to review.

Also, take a look at this great website. It has forms and civil procedures specific to your State.

Customizing Your Wrongful Foreclosure Civil Action

Please go to Documents and refer to: 004-Wrongful Foreclosure Action.doc

Watch the following video about how you would fill out the complaint. Be warned. You are filling out this complaint at your own risk. We make no assurances whatsoever as to the validity, legal sufficiency nor the completeness of this document. You are to seek competent legal counsel before submitting these documents to court.

Now customize and fill out the Wrongful Foreclosure Action. Be sure to include/enclose all the exhibits as suggested as part of your evidence packet. Remember, without sufficient evidence, your case is subject to dismissal.

After you are done, contact your study buddy and submit the document for their review. See if they have any suggestions, and ideas to help you. If you haven’t done so, please fill out your contact information at:https://www.consumerdefenseprograms.com/resources/local-meet-ups/

If you are not willing to put your name on this list, then don’t bother asking for help. Before you can receive help, you must be willing to give help. We’re all here to help each other.

After you are fully satisfied with the pleading, you should consult an attorney to get their advice. You can find an attorney here. If one is not listed, it means we don’t have anyone we can recommend in your state. Please don’t email us to ask. Try to find a lawyer locally.

Request for Admissions

Please find the Request for Admissions document and customize that to fit your needs. 004c-Request for Admissions.doc

Check with your Rules of Civil Procedures to see if you can submit it with your complaint (ie. file your complaint and include this at the same time). You should be able to. Otherwise, check with Prepaid Legal.

This is a powerful document. Your Lender needs to respond to these admissions within 30 days or the fully admit to all the accusations. Take a look at the allegations within the Request for Admissions. It will make a whole lot more sense.

In a civil action, the burden of proof is with the plaintiff. It is your job to provide as much concrete evidence as possible to support your civil action. Remember, the court is not moved by theories, conjectures and allegations. The courts are moved by

a) The Law

b) Evidence

It is your job to bring these to the judge’s attention. Anything else is useless chatter and will be dismissed. That said, you should be prepared to stand by everything you present to the court. If required, you should be willing to defend your points. So, you better know what you are doing before submitting your civil action. Once you proceed, the clock starts ticking. My advice to you is to do your homework first. Be prepared. Don’t sign/write/submit anything you don’t believe, understand or otherwise. My template is there to guide you, but ultimately, you need to own it.

One of the points of our civil action is the bifurcation clause. To illustrate bifurcation, you have to prove that it took place. Here’s how we prove it. Let’s say you closed your loan with CountryWide. And then at a foreclosure, the Substitution of Trustee is done by ABC Trust, there is an assignment that took place here.

Country Wide -> ?? -> ABC Trust

Therefore, if we go to the county record and look up the assignment, we should see the assignment of the deed of Trust to reflect this movement. If not, we have a separation (bifurcation).

Most likely, what you will see is that there was no assignment.

Therefore, what I need you to do is to go to the county recorders office, and ask for a print out of the CERTIFIED county record for your property. We will then enter this as evidence in your civil action. This will be entered as Exhibit F in the petition.

Alternatively, you could contact a local title company and pay a small fee to have them do this for you. Ask for a “preliminary title report” from the date of closing of your loan to today. Have them certify it.

Surviving a Demurrer

It is worth reiterating. It is standard procedure for opposing counsel to do a Demurrer (Motion to Dismiss) on your case…no matter what. By standard procedure, we mean WE HAVE SEEN THEM DO IT EVERY SINGLE CASE. They would rather kick your case out of court on a technicality than to have to deal with real discovery..thus exposing their fraud. Just expect it, OK? However, that said, we want to make sure your case is as strong as possible so it can survive the Demurrer.

One of the biggest problems when you bring a case against your lender is evidence. Evidence is EVERYTHING. Remember, the Plaintiff has the burden of proof.

We have said it in the previous module, and we will say it again. Your best bet in surviving a Demurrer is to have strong evidence…and one of the best things you could do is to order a Securitization audit to prove that your loan has been securitized.

If you want to get a securitization audit, go to Module 1 for more info.

Who is the Investor?

There is a good chance Fannie Mae or Freddie Mac owns your loan. If you can find your properties here, then you can present this as evidence that your servicer (so called “lender”) is not a real party of interest. This is critical evidence to bring forth in your civil action. You must include this as a claim in your suit.

To find out whether Fannie Mae owns your note, please come here.

Freddie Mac’s database is here.

IMPORTANT: DO THIS NOW. Research whether these guys own your note. If so, then you have a crucial piece of evidence to bring to court.

Remember, the investor can not foreclose. So if the pretender lender claims that they are foreclosing on behalf of the investor…they are lying. The investor is/was not a real party of interest, nor the holder in due course.

Good News About MERS

If you have MERS, in your loan, you have cause to celebrate (to find out, look at your Deed of Trust (DoT) or Mortgage document. It should say “Mortgage Electronic Registration Systems is the nominee” somewhere on the first or second page. MERS should appear on your Deed of Trust/Mortgage on the first couple of pages.

MERS is an electronic registration system that tracks which of the THOUSANDS of shareholders are the parties of interest for your loan. Not only is this expensive to track on County record (it costs $50+ per record), it’s also almost impossible because people buy and sell shares every day on Wall St.

Let us use an analogy. There’s two “things” involved in a loan. A Deed of Trust (or Mortgage) and the promissory Note. The critical “thing” is the Note. The DoT protects the note. He who controls the note controls the DoT. He who controls the DoT controls nothing. The analogy is the Note is the dog and the DoT is the tail. He who controls the dog controls the tail. He who controls the tail does not control the dog. Read the following case law:

“In CARPTENTER V. LONGAN, 83 U.S. 271 (1872), it was ruled that:

The note and mortgage are inseparable; the former as essential, the latter as an incident. An assignment of the note carries the mortgage with it, while an assignment of the latter alone is a nullity.

All the authorities agree that the debt is the principal [Note] thing and the mortgage [Deed of Trust] an accessory. Much more.”

This is why we want to make the argument to the court to illustrate the point of “who owns the note?” He who owns the note is the real party of interest and only that person has the power to enforce the note. A servicer only has the presumption of the law. The servicer is who you would call the “pretender lender”. He did not put any of his money at risk and the money did not come from him…yet he wants to foreclose on the property so he can do it again to someone else.

If you have received a Notice of Default and a Substitution of Trustee, then you will likely see that “Mortgage Electronic Registration Systems assigns ABC Bank as the Beneficiary.” This is totally invalid as per our previous point.

A) MERS is not a real party of interest, and therefore can not assign anything.

B) Even if MERS can assign the Deed of Trust….it still does not answer “who owns the note”.

We have lot’s of cases in the “Reference” file in Module 1 (please download and read these if you haven’t already done so.). I have read literally thousands of documents and saved the very best for you in this Reference file. Within Reference, you will also see a number of cases regarding MERS. Pay particular attention to: mers-citibank-not-real-parties-CA.pdf.

Take a look at this post:http://privateaudio.homestead.com/MERS.html. It has a lot of good notations about who MERS is and what they can and can not do. This is very important for you to understand if you are going to defend your points in court.

To See if your loan is being serviced by MERS, come here: https://www.mers-servicerid.org/sis/

To make the analogy perfectly clear, imagine if you will, your County Recorder going about creating an assignment for your house and assign it to his brother.

A) This is completely illegal.

B) Your County Recorder is only responsible for recording info…he is not a real party of interest an does not have the authority to assign anything. ONLY the real party of interest (ie. you) can assign anything to do with your house to anyone else.

C) MERS is not a Lender. They are not a Beneficial party of interest.

D) If you look on your Deed of Trust, there is language specifically that says something like “Assignment of Trustee: From time to time the Lender may appoint a substitution of Trustee”. No where does it say “MERS may appoint a substitution of Trustee”. MERS is not a Lender.

E) Only a real party of interest to the promissory note can assign its interest to another party.

But MERS does this EVERY SINGLE DAY. This is completely illegal. They are relying on your ignorance. This is why you should bring this up in your Quiet Title Action if you see MERS on your Deed of Trust/Mortgage.

NOTE TO CALIFORNIANS

Please refer to the References document under /California/ProduceTheNote-CaliforniaStyle.pdf for more information. Specifically page 25 and onwards. You come to your own conclusion. Also, if you are in CA, you definitely want to study mers-citibank-not-real-parties-CA.pdf. Also, there are a number of articles relating to California you should read that you could bring up if it applies to you.

Action Items

1) Customize the Pleading for the Wrongful Foreclosure Action

Use the findings and declarations in your securitization audit to add any additional claims of fraud to your civil action.

2) Customize the Request for Admissions a

3) Connect with your study Buddy and have it reviewed.

4) Consult your Rules of Civil Procedures so you understand how it all pulls together. Specifically, look under Jurisdiction, Request for admissions, and Servicing.

5) SERIOUSLY consider joining Prepaid Legal. Don’t be an idiot.

6) Consider signing up for the Document Preparation Service.

When you file a lawsuit, your lender will ALWAYS file a motion to dismiss. They will do anything they can to get your case thrown out before it sees the light of day. Hiring this law firm prepare your documents means your documents are less likely to be dismissed. They will also have another attorney from another office do a legal challenge on the pleading against you! This means, you will have already been challenged and there is very little chance your pleading will be dismissed. You will need to survive the Demurrer (Motion to Dismiss) before you can enter discovery.

Disclaimer:

This is purely for educational purpose. Nothing on this site can be construed as giving legal advice. You are using this information at your own risk. You are to seek legal counsel in these matters.