If you live in California, you know that it is by far, one of the most corrupt and hardest states to win in a Foreclosure Defense Action. Judges have been siding with banks for years.

That just changed…as of Feb 2016.

You see, Judges have been ruling that homeowners in foreclosure basically have no right to challenge phoney/defective assignments from pretender lenders. They have gone as far to say “all fraudulent assignments does not matter”. This issue was argued all the way up to the Californian Supreme Court in re: Yvanova v. New Century Mortgage Corporation (Case No. S218973, Cal. Sup. Ct. February 18, 2016).

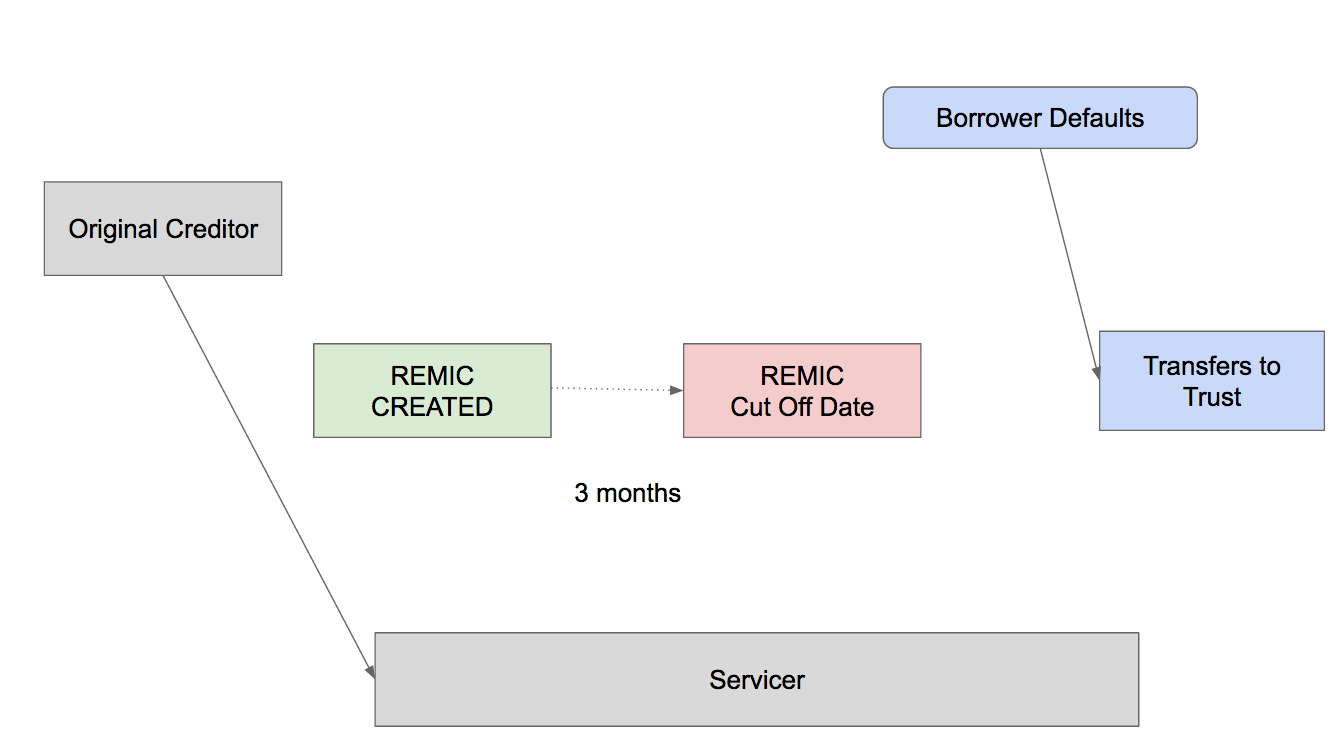

Basically, the case boils down to this. The loan was assigned to the REMIC Trust outside of the 90 days from the creation of the Trust. (IRS Tax rule on REMIC says that in order for an asset to qualify, it has to be assigned within 3 months from the creation date of the REMIC.)…not only that, it was assigned from a non existent/defunct company “New Century Mortgage”….years after it went out of business.

Take a look at this:

What should have happened was, the loan should have been assigned into the REMIC within 3 years…what actually happened was, it was only assigned into the REMIC AFTER the borrower went into default. By this time, New Century Mortgage has already gone out of business.

Here’s what the Supreme Court ruled:

“In seeking a finding that an assignment agreement was void, therefore, a plaintiff in Yvanova‘s position is not asserting the interests of parties to the assignment; she is asserting her own interest in limiting foreclosure on her property to those with legal authority to order a foreclosure sale. This, then, is not a situation in which standing to sue is lacking because its ―sole object . . . is to settle rights of third persons who are not parties. (Golden Gate Bridge etc. Dist. v. Felt (1931) 214 Cal. 308, 316.)”

This has been our position and argument all along in our Foreclosure Defense Program.

The Supreme Court further went on eloquently to say:

“Nor is it correct that the borrower has no cognizable interest in the identity of the party enforcing his or her debt. Though the borrower is not entitled to object to an assignment of the promissory note, he or she is obligated to pay the debt, or suffer loss of the security, only to a person or entity that has actually been assigned the debt. (See Cockerell v. Title Ins. & Trust Co., supra, 42 Cal.2d at p. 292 [party claiming all components listed under an assignment must prove fact of assignment].) The borrower owes money not to the world at large but to a particular person or institution, and only the person or institution entitled to payment may enforce the debt by foreclosing on the security.”

This is a HUGE DEAL for homeowners across the country. This is something that you can now start using to defend your home against foreclosure.

To learn how you can fight foreclosure and stop the bank dead cold in its tracks, join our free 55 minute webinar. It is JAMMED PACKED WITH all the legal remedies you can use to expose the fraud being committed by banks every day. Don’t let them steal your house.